The Annual Members’ Assembly of Confindustria Nautica – the Italian Marine Industry Association, held on 11 December 2025 in Rome at Montecitorio Palace, the seat of the Chamber of Deputies of the Italian Parliament, offered a detailed and nuanced snapshot of the current state of Italy’s boating industry. The outlook, developed by the Association’s Research Department and based on a survey conducted during the first week of December among a representative sample of member companies, confirms a sector in a phase of consolidation – yet far from lacking momentum or perspective.

“Something significant happened in 2024: exports from the recreational boating industry surpassed those of the entire commercial shipbuilding sector, reaching an all-time high in both revenues and employment. If it ever was the case, the time when boating was considered a secondary industry – within Italian manufacturing and the wider economy – is definitively over,” said Piero Formenti, President of Confindustria Nautica, in his opening remarks.

Superyachts: solid performance amid slowing growth rates

The superyacht segment closes 2025 on a decidedly positive note. Half of the companies surveyed forecast an increase in turnover compared to the previous year, while a further 25% expect stable results. Order books point to a normalisation of growth after the exceptional years behind us: 50% of shipyards report order books in line with those of 12 months ago, while another 25% show further expansion.

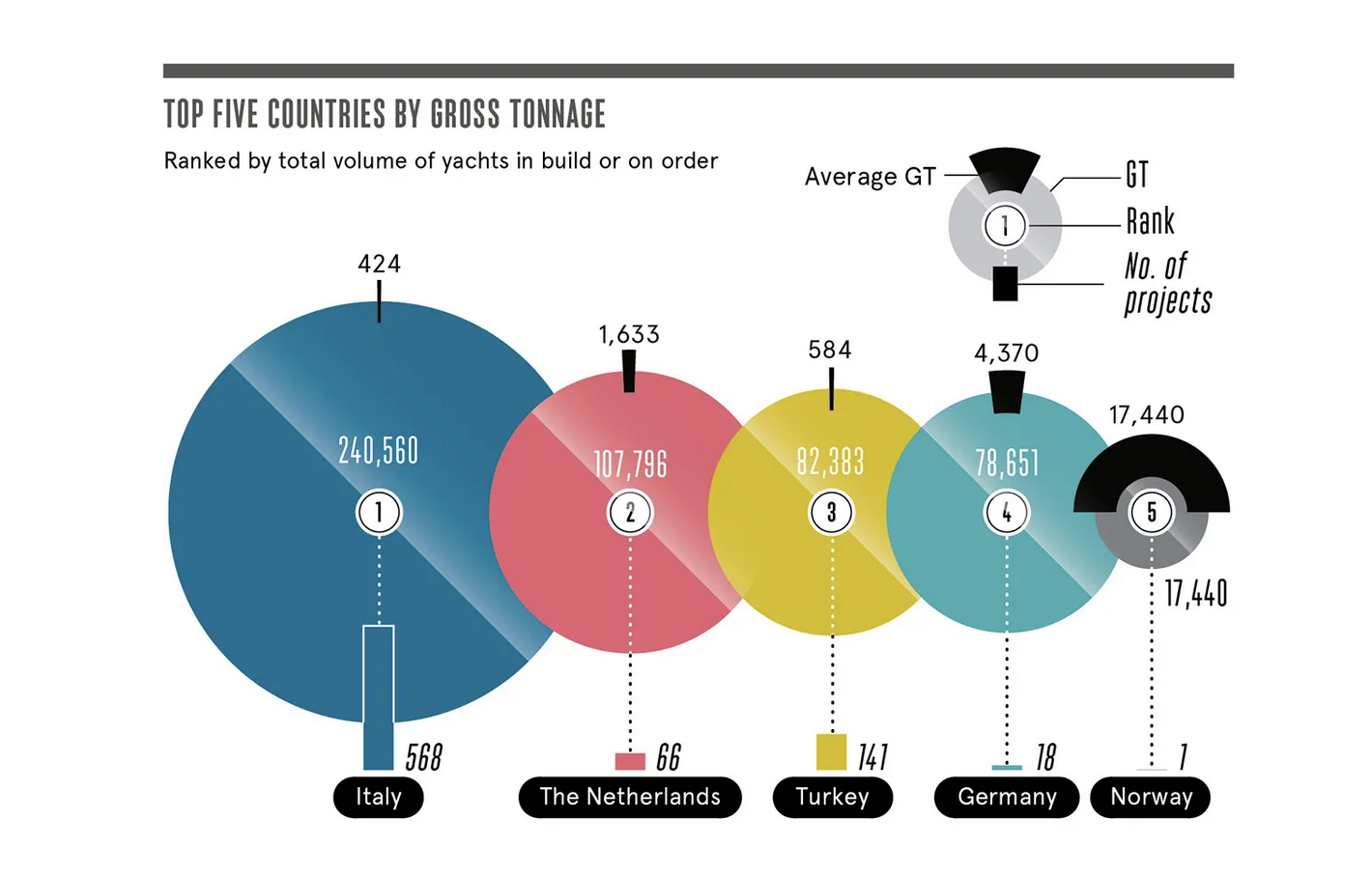

This trend is echoed by Boat International’s preview of the 2026 Global Order Book. Although global orders decline from 1,138 to 978 units, Italy strengthens its leadership, increasing its market share by nearly three percentage points to reach 53% of global production.

Under 24 m: a more complex landscape, but improving prospects

The picture is more articulated for boatbuilding up to 24 m – including motorboats, sailing yachts and inflatables. End-of-year estimates for 2025 indicate a decline in turnover for 54% of respondents, with reductions ranging from -5% to over -30%. Stability and growth are each reported by 23% of companies, broadly mirroring the situation observed in 2024.

Looking ahead to the 2025/26 nautical year, however, sentiment improves: 46% of companies expect growth, 31% foresee stable revenues and only 23% anticipate a contraction.

Sales Networks: confidence gradually returning

A similar shift emerges from the recreational boat sales network. While 2025 is set to close with negative forecasts for 62% of the sample and stable results for the remaining 38%, expectations for the current nautical year are notably more upbeat. The share of respondents forecasting a downturn drops to 37%, while 50% expect stability and 13% anticipate a reversal of the trend, with turnover growth returning.

Marine Engines: stability with upward signals

In the marine engines segment, 2025 shows an evenly balanced picture: 25% of companies expect growth, 25% a decline and 50% stable revenues. Sentiment improves for the current nautical year, with the proportion of companies forecasting stability unchanged at 50%, while those expecting growth rise to 37%.

Components and Equipment: a highly diversified outlook

Preliminary figures for components and equipment reveal a highly diversified scenario. Forty percent of companies report stable turnover compared to 2024, while the remaining 60% is evenly split between growth (up to +20%) and contraction (between -5% and -30%).

As already seen last year, this dispersion reflects the strong heterogeneity of product categories and end markets – ranging from superyachts to small craft and aftersales. Forecasts for the 2025/26 nautical year show a similar distribution, but with an encouraging signal: positive expectations increase from 30% to 39%.

Leasing and Charter: a clearly positive trend

The leasing and charter sector stands out with particularly strong results. In 2025, 57% of companies report turnover growth – exceeding +20% in some cases – while 14% record stability and 29% a limited decline, contained within a -10% range.

Outlook for the current nautical year is decidedly optimistic: 64% of respondents expect growth, 29% stability and just 7% foresee a possible downturn.

A global context in transformation

The future of Italy’s recreational boating industry unfolds within a global landscape undergoing profound transformation. According to Professor Gabriele Natalizia, Chair of Political Science and International Security, who opened the Assembly with an in-depth analysis of US strategic priorities, the current trajectory of the American administration is fully consistent with policies set in motion as early as 2009 and carried forward across successive governments.

This long-term strategic line pursues objectives that include burden sharing, a reduction of non-vital international commitments, and a decisive reorientation towards the Indo-Pacific region.

“This is a trend destined to endure over the long term,” Natalizia explained, “as it is instrumental to economic and military competition with China. As a result, companies and industrial supply chains are being called upon to undertake structural adjustments that cannot be interpreted as short-term contingencies.”

Outlook: early signs of recovery for 2026–2027

Overall, the scenario confirms the assumptions outlined last September during the presentation of the statistical report La Nautica in Cifre LOG (“Boating in Figures”), also discussed in Nautech’s November 2025 issue. The first signs of the recovery expected for 2026–2027 have already become visible at recent autumn trade shows, starting with the 65th Genoa International Boat Show.

New product launches, a strong focus on emerging trends and evolving market demands, and renewed confidence among small boat owners have helped reinforce the sector, while further consolidating the strength of the large yacht segment. Despite ongoing geopolitical and macroeconomic uncertainties, forecasts for the current nautical year remain encouraging for the Italian boating industry and its entire supply chain.