On 17 September, on the eve of the 65th Genoa International Boat Show, the Forum Hall of the Blue Pavilion hosted one of the most eagerly awaited events: the presentation of the new Boating Economic Forecast, with updated figures for the Italian recreational boating industry.

At the heart of the conference was the new edition of Nautica in Cifre – LOG, the only officially recognised statistical report in the sector, produced by the Research Department of Confindustria Nautica in collaboration with the Edison Foundation.

The event confirmed the double vocation of the Genoa Boat Show: not only a global showcase for new products, but also a strategic platform for assessing the state of the industry and outlining its future prospects, consolidating the position of Italian yachting as one of the crown jewels of national manufacturing, particularly thanks to evolving Yacht Market Trends.

2024: record turnover

The figures are clear: a total turnover of 8.60 billion euros in 2024, +3.2% compared to the previous year. This result marks the consolidation of an unprecedented growth cycle that has seen the sector double in size in just four years since the post-pandemic recovery.

“The 2024 results for the recreational marine industry are positive: the sector’s turnover has grown by 3.2%, reaching an all-time high of €8.60 billion,” said Piero Formenti, President of Confindustria Nautica, in his opening remarks.

“Growth has been driven by the high-end segment and superyachts, which continue to lead the world market, while small boatbuilders have seen a decline of around -10%. The difficulties in this segment are due to a combination of factors, including excess inventory in certain markets, rising geopolitical tensions, weaker consumer confidence and a domestic regulatory framework that is still burdened by bureaucracy.”

The picture that emerges is of a resilient but polarised sector, with large yachts and luxury shipyards driving growth, while smaller boatbuilders face structural and cyclical headwinds.

Exports, the lifeblood of the industry

Among the main growth drivers, export performance once again stands out: 70.3% of total turnover (around €6.05 billion) was generated abroad, compared to a domestic market worth €2.55 billion (29.7%).

The most significant figure comes from new buildings: 89% of the units produced in Italy are delivered to international clients, consolidating the country’s leadership in global yacht and boatbuilding.

“In 2024, Italy confirmed its position as the world’s leading exporter in the recreational boatbuilding industry,” emphasised Marco Fortis, Director and Vice President of Fondazione Edison. “Exports of ‘pleasure and sports boats’ exceeded €4.3 billion (+7.5% compared to 2023), with an export propensity of around 90% of domestic production. The US remains a key market – especially for boats under 24 m – although tariff uncertainties have affected orders. This highlights the need to diversify export destinations and use international boat shows as business platforms and gateways for new partnerships.”

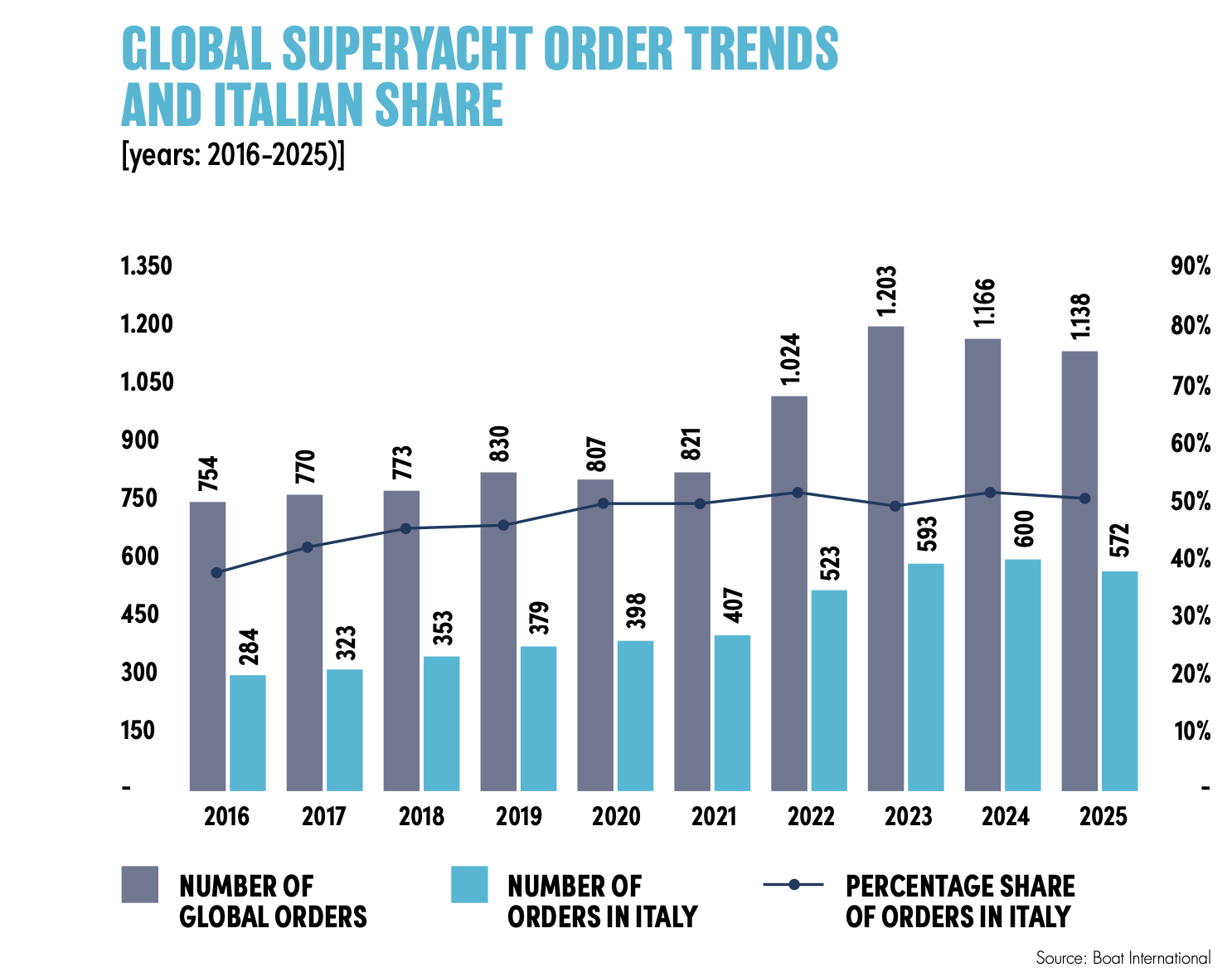

Here the Superyacht Industry plays a decisive role

Another emblematic figure comes from the Global Order Book 2024, published by Showboats International: Italy tops the global ranking with 572 superyachts under construction, representing 50% of the world’s total orders.

Turkey, in second place, is a distant third with 146 yachts, followed by the UK (81) and the Netherlands (69). The total length of Italian yachts under construction exceeds 22,000 m, a figure that speaks volumes about the supremacy of Italian shipyards in this market segment.

According to the Nautica in Cifre – Monitor 2024/2025, this concentration of orders confirms the role of the superyacht sector as the driving force of the industry but also signals the first signs of stabilisation: the order volume registered a slight decrease of -4.6% compared to 2023.

Small boats: signs of strain

While the high-end market is booming, the small boat sector is showing signs of strain. Surveys carried out by Confindustria Nautica show that 60% of companies building boats under 24 m expect their turnover to fall, with only a small minority forecasting growth.

“Based on the sentiment of leading Italian operators, the difficulties in small boat building, combined with the uncertainty of the US tariffs, could trigger a global slowdown in 2025,” explains Stefano Pagani Isnardi, Director of the Research Department at Confindustria Nautica. “However, entrepreneurs expect a recovery between 2026 and 2027. The first signs of this turnaround could already be seen at our Genoa International Boat Show, where new models and attention to evolving market trends could rekindle owners’ confidence.”

The Monitor highlights the most critical factors weighing on the sector: high interest rates, persistent inflation, geopolitical tensions and excess inventory, particularly affecting SMEs.

Employment and contribution to GDP

Far from being a niche sector, the Italian yachting industry provided employment for 31,480 people in 2024 (+2.6% compared to 2023) and contributed €7.40 billion to Italy’s GDP, equivalent to 0.337% of the national total.

This makes recreational boating one of the country’s most profitable manufacturing sectors, alongside fashion and agri-food, and confirms its role as a strategic pillar of the Made in Italy economy.

Nautical tourism and marina services: post-Covid normalisation

The growth of NauticalTourism continues to influence marina services and charter trends.

In addition to manufacturing, nautical tourism and marina services continued their positive trend, albeit with more moderate growth compared to the immediate post-pandemic boom.

• Permanent moorings: +2%

• Transient moorings: +2.3%

• Revenue from storage: +3.2%

• Maintenance services: +2%

• Fuel sales: +1.6%

• Ancillary services: +2.3%

In the charter market, expectations for 2025 remain positive: 50% of operators forecast revenue growth, 47% expect stability and only 7% foresee a slight decline. The demand for experiential boating holidays, increasingly focused on sustainability, is consolidating as a long-term trend.

Exports: a twenty-year success story

Between 2000 and 2024, exports of recreational and sports boats will grow from €850 million to €4.3 billion, an extraordinary increase of +405.8%.

This makes the sector one of the most dynamic of Italy’s manufacturing surplus industries. In fact, recreational boating now ranks 5th in terms of export growth among manufacturing sectors with a trade surplus of over €2 billion, competing with much larger industries.

Looking ahead: challenges and opportunities

The international outlook remains complex: global GDP growth is forecast at 3.2%, the Eurozone lags at +0.8% in 2024, while global trade faces headwinds and US trade policy adds uncertainty.

For the Italian yachting industry, the challenge is twofold: to consolidate its leadership in the luxury segment and to revitalise small boatbuilding through innovation, sustainability and regulatory simplification.

As Pagani Isnardi pointed out, a recovery could take place as early as 2026/2027, driven by new model launches and renewed confidence among yacht owners.

The year 2024 will be remembered as a milestone for the Italian yachting industry: record turnover, world leadership in yacht building and continued export growth. But the Genoa Boat Show also highlighted the challenges ahead: supporting small boatbuilders, navigating geopolitical turbulence and diversifying export markets.

As Marco Fortis emphasised, international boat shows remain fundamental business and networking platforms. Once again, the Genoa International Boat Show proved to be not only the “home of Italian yachting”, but also a barometer of an industry that looks to the future with confidence, fully aware of the challenges it faces.

Who are today’s Italian yacht owners?

The 65th Genoa International Boat Show was also the venue for the first in-depth analysis of the profile of Italian yacht and boat owners. The study – carried out by the National Nautical Observatory of Confindustria Nautica and presented by Roberto Neglia, Head of Institutional Relations and Coordinator of the Observatory – provides the most accurate snapshot to date of the Italian recreational boating community.

For the first time, socio-demographic data (age, gender, place of residence) has been cross-referenced with yacht specifications (size, engine, year of construction, type of unit) and territorial specificities. This analysis of Italian yacht ownership reveals a sector that is mature, metropolitan and largely driven by older generations, but with encouraging signs of change.

The report is a strategic tool to guide public policy and industry decisions that are essential to accompany Italian yachting towards a more inclusive and competitive future and provides valuable insights for industry stakeholders and policy makers alike:

• The generation gap highlights the need to attract younger owners through innovative access models such as charter, fractional ownership and green propulsion.

• The growing role of women offers opportunities for cultural and market renewal.

• The lag in new registrations points to regulatory and infrastructure shortcomings that need to be addressed to support a sustainable expansion of the sector.

A mature but polarised sector

The data underlines the maturity of the market: 80% of Italian yacht owners are over 50 years old, with a strong concentration in the 60-75 age group (45% of the total). Women are still a minority (13%), but their share is growing and they are on average younger than their male counterparts.

The typical Italian boat owner is therefore male, aged between 60 and 75, living in a metropolitan area (mainly Rome or Milan) and owning a 10-12 metre inboard motorboat built between 2000 and 2009.

Younger owners: still a niche, but a strategic one

Although limited in number, yacht owners under the age of 40 represent a key segment for generational renewal. The south of Italy leads with over 25% of all young owners, followed by the north-east (18%). Cities such as Naples, Rome and Trieste have above average figures. Conversely, the 20-29 and under-20 age groups remain marginal, below 5% nationally, although some urban centres are above average.

A metropolitan phenomenon

The geographical distribution is balanced: North-East 25%, Centre 24%, North-West 21%, South 20%, Islands 10%. The top ten municipalities by number of yacht owners confirm the predominance of large cities: Rome, Milan and Naples together account for about 1/3 of the total. They are followed by Trieste, Genoa, Turin, Venice, Padua, Palermo and Florence.

This confirms that recreational boating in Italy is a predominantly metropolitan phenomenon and is not limited to coastal communities.

Fleet profile: age and propulsion

The Italian fleet remains relatively old: 35% of the units were built before 2000 and less than 10% after 2020. Inboard engines are by far the most common choice (73%), especially among owners aged 60-75.

Sailing yachts show a more balanced distribution across generations, appealing to a wider and more diverse audience.

In terms of installed power, the most common category is 251-999hp (35%), followed by 40-115hp (22%).

Berths and flag registration

The availability of moorings is under pressure in the Centre-North and in the province of Naples, while the south is underserved in terms of temporary moorings.

On the registration front, only 2% of yacht owners are foreign residents, either EU or non-EU nationals, confirming the largely domestic profile of the Italian flag.

Registrations: the weak link

The analysis highlights a long-standing structural problem: new registrations. After peaking in 2006 with more than 800 new boats per year, registrations collapsed between 2012 and 2014 – falling below 200 per year – due to the global financial crisis and domestic fiscal measures such as the so-called ‘Monti tax’.

Since 2015, the sector’s turnover has steadily recovered, reaching a record €8.6 billion in 2024, but registrations have grown only marginally and remain at historically low levels compared to the mid-2000s.